C H A P T E R O N E

Four Basic Misconceptions About Money

EVERY DAY almost everyone on this planet uses money. Yet few people understand how money works and affects their lives directly and indirectly. Let us, therefore, take a closer look at what money is and what would happen without it. First, the good news: Money is one of the most ingenious inventions of humankind, as it helps the exchange of goods and services and overcomes the limits of barter, that is, the direct exchange of goods and services. For example, if you live in a village which relies entirely on barter, and you produce works of art but there is nobody to exchange your artwork with except the undertaker, you will soon have to change your occupation or leave. Thus, money creates the possibility for specialization, which is the basis of civilization. Then why do we have a "money problem"? Here comes the bad news: Money does not only help the exchange of goods and services but can also hinder the exchange of goods and services by being kept in the hands of those who have more than they need. Thus it creates a private toll gate where those who have less than they need pay a fee to those who have more money than they need. This is by no means a "fair deal." In fact, our present monetary systems could be termed "unconstitutional" in most democratic nations, as I will show later. Before going into more detail let me say that there are probably more than just four misconceptions about money. Our beliefs about money represent a fairly exact mirror of our beliefs about the world in which we live, and those are as varied as the number of people who live on this planet. However, the four misconceptions which will be discussed in the following pages are the most common hindrances to understanding why we must change the present money system and what mechanisms we need in order to replace it.

First Misconception

THERE IS ONLY ONE TYPE OF GROWTH

The first misconception relates to growth. We tend to believe that there is only one type of growth, that is, the growth pattern of nature which we have experienced ourselves. Figure 1, however, shows three generically different patterns:

Curve A represents an idealized form of the normal physical growth pattern in nature which our bodies follow, as well as those of plants and animals. We grow fairly quickly during the early stages of our lives, then begin to slow down in our teens, and usually stop growing physically when we are about twenty-one. This, however, does not preclude us from growing further "qualitatively" instead of "quantitatively." Curve B represents a mechanical or linear growth pattern, e.g., more machines produce more goods, more coal produces more energy. It comes to an end when the machines are stopped, or no more coal is added. Curve C represents an exponential growth pattern which may be described as the exact opposite to curve A in that it grows very slowly in the beginning, then continually faster, and finally in an almost vertical fashion. In the physical realm, this growth pattern usually occurs where there is sickness or death. Cancer, for instance, follows an exponential growth pattern. It grows slowly first, although always accelerating, and often by the time it has been discovered it has entered a growth phase where it cannot be stopped. Exponential growth in the physical realm usually ends with the death of the host and the organism on which it depends. Based on interest and compound interest, our money doubles at regular intervals, i.e., it follows an exponential growth pattern. This explains why we are in trouble with our monetary system today. Interest, in fact, acts like cancer in our social structure.

Figure 2 shows the time periods needed for our money to double at compound interest rates: at 3%, 24 years; at 6%, 12 years; at 12%, 6 years. Even at 1% compound interest, we have an exponential growth curve, with a doubling time of 72 years. Through our bodies we have only experienced the physical growth pattern of nature which stops at an optimal size (Curve A). Therefore, it is difficult for human beings to understand the full impact of the exponential growth pattern in the physical realm. This phenomenon can best be demonstrated by the famous story of the Persian emperor who was so enchanted with a new chess game that he wanted to fulfill any wish the inventor of the game had. This clever mathematician decided to ask for one seed of grain on the first square of the chess board doubling the amounts on each of the following squares. The emperor, at first happy about such modesty, was soon to discover that the total yield of his entire empire would not be sufficient to fulfill the "modest" wish. The amount needed on the 64th square of the chess board equals 440 times the yield of grain of the entire planet. (1) A similar analogy, directly related to our topic, is that one penny invested at the birth of Jesus Christ at 4% interest would have bought in 1750 one ball of gold equal to the weight of the earth. In 1990, however, it would buy 8,190 balls of gold. At 5 % interest it would have bought one ball of gold by the year 1466. By 1990, it would buy 2,200 billion balls of gold equal to the weight of the earth. (2) The example shows the enormous difference 1 % makes. It also proves that the continual payment of interest and compound interest is arithmetically, as well as practically, impossible. The economic necessity and the mathematical impossibility create a contradiction which in order to be resolved has led to innumerable feuds, wars and revolutions in the past.

The solution to the problems caused by present exponential growth is to create a money system which follows the natural growth curve. That requires the replacement of interest by another mechanism to keep money in circulation. This will be discussed in detail in Chapter 2.

Second Misconception

WE PAY INTEREST ONLY IF WE BORROW MONEY

A further reason why it is difficult for us to understand the full impact of the interest mechanism on our monetary system is that it works in a concealed way. Thus the second common misconception is that we pay interest only when we borrow money, and, if we want to avoid paying interest, all we need to do is avoid borrowing money.

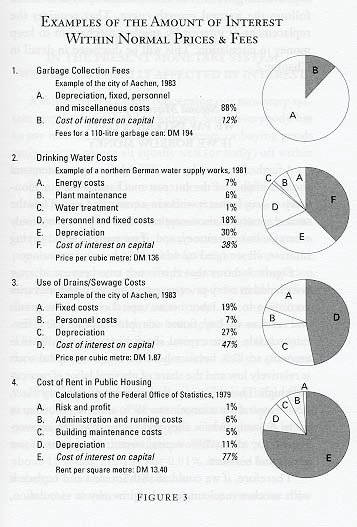

Figure

3 shows that this is not true because interest is included in every price we

pay. The exact amount varies according to the labor versus capital costs of

the goods and services we buy. Some examples indicate the difference clearly.

The capital share in garbage collection amounts to 12 % because here the share

of capital costs is relatively low and the share of physical labor is particularly

high. This changes in the provision of drinking water, where capital costs amount

to 38 %, and even more so in social housing, where they add up to 77 %. On an

average we pay about 50% capital costs in the prices of our goods and services.

Therefore, if we could abolish interest and replace it with another mechanism

to keep money in circulation, most of us could either be twice as rich or work

half of the time to keep the same standard of living we have now.

Figure

3 shows that this is not true because interest is included in every price we

pay. The exact amount varies according to the labor versus capital costs of

the goods and services we buy. Some examples indicate the difference clearly.

The capital share in garbage collection amounts to 12 % because here the share

of capital costs is relatively low and the share of physical labor is particularly

high. This changes in the provision of drinking water, where capital costs amount

to 38 %, and even more so in social housing, where they add up to 77 %. On an

average we pay about 50% capital costs in the prices of our goods and services.

Therefore, if we could abolish interest and replace it with another mechanism

to keep money in circulation, most of us could either be twice as rich or work

half of the time to keep the same standard of living we have now.

Third Misconception

IN THE PRESENT MONETARY SYSTEM WE ARE ALL EQUALLY AFFECTED BY INTEREST

A third misconception concerning our monetary system may be formulated as follows: Since everybody has to pay interest when borrowing money or buying goods and services, we are all equally well (or badly) off within our present monetary system. Not true again. There are indeed huge differences as to who profits and who pays in this system.

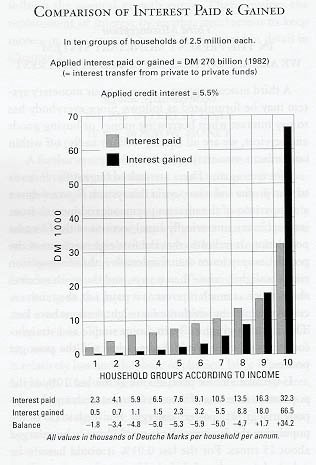

Figure

4 shows a comparison of the interest payments and income from interest in ten

numerically equal sections of the German population. It indicates that the first

eight sections of the population pay more than they receive, the ninth section

receives slightly more than it pays, and the tenth receives about twice as much

interest as it pays, i.e., the tenth receives the interest which the first eight

sections have lost. This explains graphically, in a very simple and straightforward

way, why "the rich get richer and the poor get poorer."

Figure

4 shows a comparison of the interest payments and income from interest in ten

numerically equal sections of the German population. It indicates that the first

eight sections of the population pay more than they receive, the ninth section

receives slightly more than it pays, and the tenth receives about twice as much

interest as it pays, i.e., the tenth receives the interest which the first eight

sections have lost. This explains graphically, in a very simple and straightforward

way, why "the rich get richer and the poor get poorer."

If we take a more precise look at the last 10% of the population in terms of income from interest, another exponential growth pattern emerges. For the last 1 % of the population the income column would have to be enlarged about 15 times. For the last 0.01 % it would have to be enlarged more than 2,000 times. In other words, within our monetary system we allow the operation of a hidden redistribution mechanism which constantly shuffles money from those who have less money than they need to those who have more money than they need. This is a different and far more subtle and effective form of exploitation than the one Marx tried to overcome. There is no question, that he was right in pointing to the source of the "added value" in the production sphere. The distribution of the "added value," however, happens to a large extent in the circulation sphere. This can be seen more clearly today than in his time. Ever larger amounts of money are concentrated in the hands of ever fewer individuals and corporations. For instance, the cash flow surplus, which refers to money floating around the world to wherever gains may be expected from changes in national currency or stock exchange rates, has more than doubled since 1980. The daily exchange of currencies in New York alone grew from $18 billion to $50 billion between 1980 and 1986. (3) The World Bank has estimated that money transactions on a world wide scale are from 15 to 20 times greater than necessary for financing world trade. (4) The interest and compound interest mechanism not only creates an impetus for pathological economic growth but, as Dieter Suhr has pointed out, it works against the constitutional rights of the individual in most countries. (5) If a constitution guarantees equal access by every individual to government services and the money system may be defined as such then it is illegal to have a system in which 10% of the people continually receive more than they pay for that service at the expense of 80% of the people who receive less than they pay. It may seem as if a change in our monetary system would serve "only" 80% of the population, i.e., those who at present pay more than their fair share. However, I will show in Chapter 3 that everybody profits from a cure, even those who profit from the cancerous system we have now.

Fourth Misconception

INFLATION IS AN INTEGRAL PART OF FREE MARKET ECONOMIES

A fourth misconception relates to the role of inflation in our economic system. Most people see inflation as an integral part of any money system, almost "natural," since there is no capitalist country in the world with a free market economy without inflation.

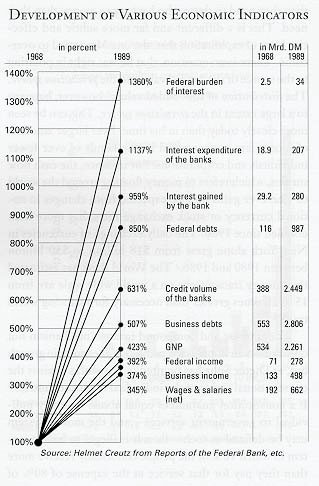

Figure

5, Development of Various Economic Indicators, shows some of the factors that

may cause inflation. While the governmental income, the Gross National Product,

and the salaries and wages of the average income earner "only" rose

by about 400% between 1968 and 1989, the interest payments of the government

rose by 1,360%.

Figure

5, Development of Various Economic Indicators, shows some of the factors that

may cause inflation. While the governmental income, the Gross National Product,

and the salaries and wages of the average income earner "only" rose

by about 400% between 1968 and 1989, the interest payments of the government

rose by 1,360%.

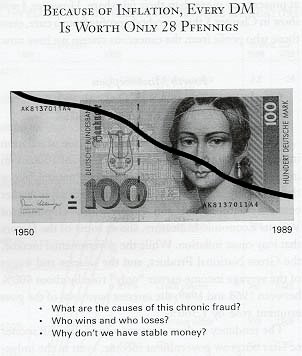

The tendency is clear government debts will sooner or later outgrow government income, even in the industrialized nations. If a child grew three times its size, say, between the ages of one and nine, but its feet grew to eleven times their size, we would call it sick. The problem here is that very few people care to see the signs of sickness in the monetary system, even fewer people know a remedy, and nobody has been able to set up a "healthy" working model which has lasted. Few realize that inflation is just another form of taxation through which governments can somewhat overcome the worst problems of increasing debt. Obviously, the larger the gap between income and debt, the higher the inflation needed. Allowing the central banks to print money enables governments to reduce debts. Figure 6 shows the reduction of the value of the DM between 1950 and 1989. This devaluation hit that 80% of the people hardest who pay more most of time. They usually cannot withdraw their assets into "inflation-resistant" stocks, real estate or other investments like those who are in the highest 10% income bracket.

Economic historian, John L. King, links inflation to the interest paid for the "credit balloon." In a private letter to me, dated January 8, 1988, he states: I have written extensively about interest being the major cause of rising prices now since it is buried in the price of all that we buy, but this idea, though true, is not well accepted. $9 trillion in domestic U.S. debt, at 10% interest, is $900 billion paid in rising prices and this equates to the current 4% rise in prices experts perceive to be inflation. I have always believed the compounding of interest to be an invisible wrecking machine, and it is hard at work right now. So we must get rid of this mindless financial obsession. A 1,000% expansion of private and public debt occurred in the U.S.A. during the last 33 years, the largest share coming from the private sector.

But every resource of the Federal Government was utilized to spur this growth: loan guarantees, subsidized mortgage rates, low down-payments, easy terms, tax credits, secondary markets, deposit insurances, etc. The reason for this policy is that the only way to make the consequences of the interest system bearable for the large majority of the population is to create an economic growth which follows the exponential growth rate of money a vicious circle with an accelerating, spiraling effect. Whether we look at inflation, social equity, or environmental consequences, it would seem sensible from many points of view to replace the "mindless financial obsession" with a more adequate mechanism to keep money in circulation.